Bombay HC Condones Delay In Stamp Duty Refund Application

- September 05, 2024

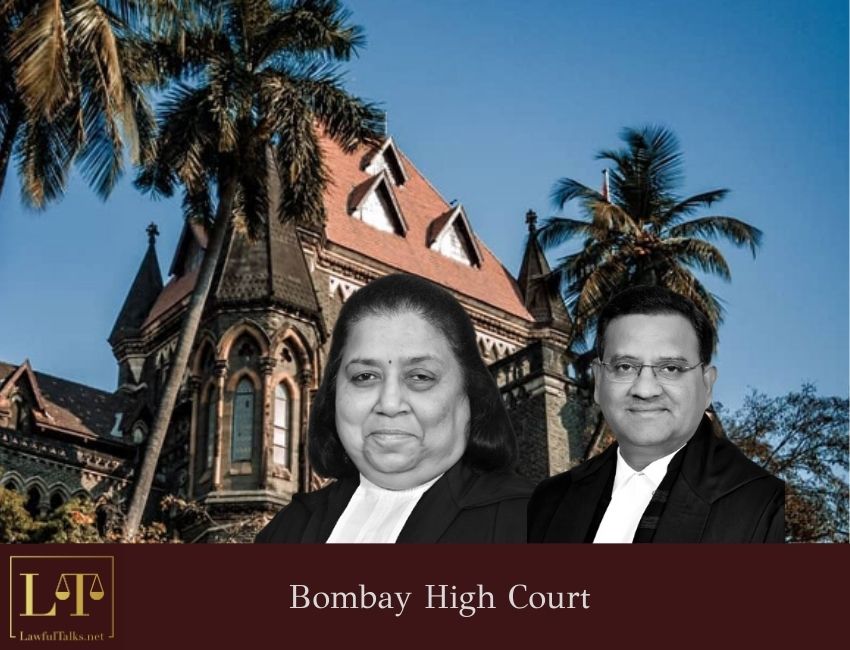

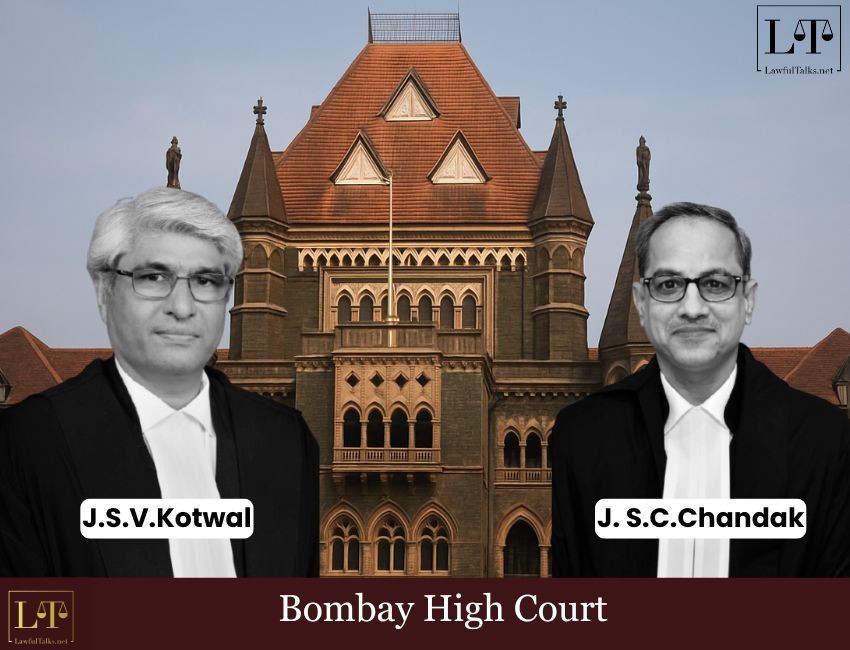

Recently the Bombay High Court Bench, presided by Justice K. R. Shriram and Justice Jitendra Jain, addressed an issue concerning the refund of stamp duty under the Maharashtra Stamp Act, 1958. The petitioner, sought the court’s intervention after his application for a refund of stamp duty was rejected by the authorities on the grounds of being filed beyond the prescribed period. The court ultimately ruled in favour of condoning the delay and allowed the refund application to be reconsidered on its merits.

The case revolved around a development agreement entered into by the petitioner on March 3, 2014, with Keshav Krishanlal Syngal, for which the petitioner paid a substantial stamp duty of ₹78,65,000. This agreement was duly registered on the same day. Later, on July 4, 2014, a supplementary agreement was executed and registered, on payment of stamp duty of Rs.300/- and registration fees of Rs.1,720/-, further formalizing the terms of the original agreement. However, the parties eventually decided to cancel the development agreement, leading to the execution and registration of a cancellation deed on June 26, 2015. Subsequently, the petitioner and Syngal entered into a conveyance deed on June 25, 2015, which was also registered, this time with a stamp duty payment of ₹1 crore.

On February 15, 2018, nearly three years after the cancellation, the petitioner applied for a refund of the ₹78,65,000 stamp duty paid on the development agreement. The application was rejected by the Inspector General of Registrar and Controller of Stamps on July 3, 2018, on the grounds that it was filed 2 years, 7 months, and 20 days late, far beyond the six-month period stipulated under Section 48(1) of the Maharashtra Stamp Act, 1958.

The petitioner’s counsel, Mr. Reis, argued that the government had effectively collected stamp duty twice for the same property and transaction, amounting to unjust enrichment. He contended that the government was only entitled to the ₹1 crore paid on the conveyance deed and that retaining the additional ₹78,65,000 was inequitable. The rejection of the refund application on the grounds of technical delay, he argued, ignored the substantive merits of the case.

In support of his argument, Mr. Reis cited the Supreme Court’s decision in Bano Saiyed Parwad vs. Chief Controlling Revenue Authority and Inspector General of Registration and Controller of Stamps & Ors. 2024 SCC OnLine SC 979, where it was held that “when the State deals with a citizen it should not ordinarily rely on technicalities, and if the State is satisfied that the case of the citizen is a just one, even though legal defenses may be open to it, it must act, as an honest person.”

The Division Bench examined the provisions of Section 48 of the Maharashtra Stamp Act, which prescribes a six-month period for filing refund applications. However, the court noted, “Though it does provide an outer limit of 6 months to make the application from the date of instruments, it does not say that application made beyond the period of 6 months will not be entertained.” The court further observed that the Stamp Act does not confer any power to condone delay on the authorities, suggesting that such discretion is reserved for the courts under Article 226 of the Constitution of India.

The court relied on case Mool Chandra vs. Union of India & Anr. 2024 SCC OnLine SC 1878 where the Apex Court has observed that it is not the length of delay that would be required to be considered while examining the plea for condonation of delay, it is cause for delay which has been propounded will have to be examined. If the cause for delay would fall within the four corners of “sufficient cause”, irrespective of length of delay same deserves to be condoned.

The court acknowledged the petitioner’s justifiable reasons for the delay, noting that the petitioner had been ill-advised, which led to the late filing. Invoking Section 5 of the Limitation Act, 1963, the court held that the delay could be condoned in the interests of justice, allowing the refund application to be reconsidered on its merits. The court remarked, “In our view, the present petition can be treated as an application under Section 5 of the Limitation Act, which provides that any application may be admitted after the prescribed period if the applicant satisfies the Court that he had sufficient cause for not making the application within the period specified.”

In light of the following arguments, the bench quashed and set aside the impugned order dated July 3, 2018, and remanded the matter to the Inspector General of Registrar and Controller of Stamps denovo consideration on merits only.

Case Details- Nanji Dana Patel v. State of Maharashtra

W/P:1897 OF 2019

Advocate for Petitioner- Mr. Bernardo Reis i/b. Mr. Shailesh Rai

Advocate for Respondents- Mr. Shahaji Shinde, A Panel Counsel a/w Mr. Sandip Babar, AG

Sign up for free and be the first to get notified about curated content just for you.