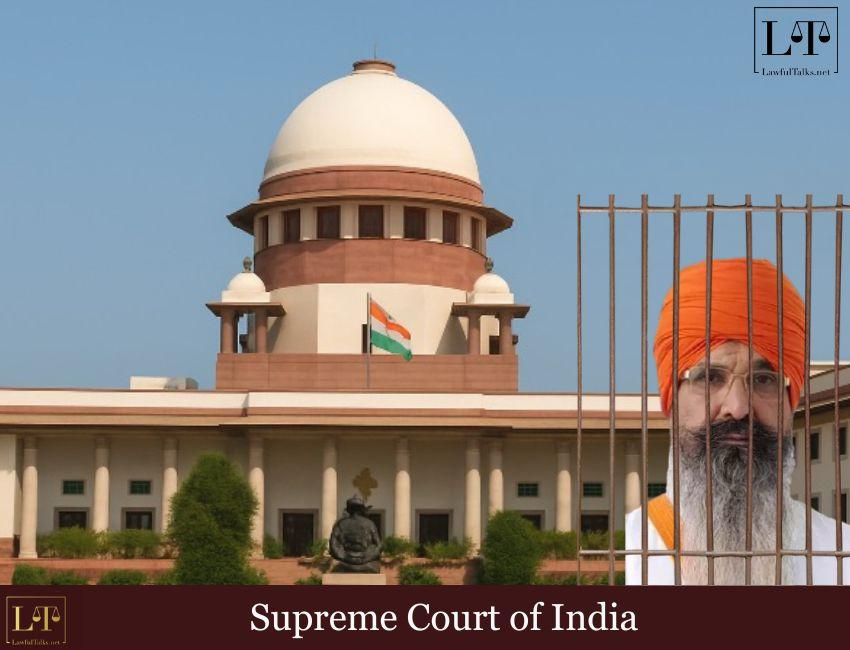

SC Calls Out ‘Afterthought’ Defences : Overturns NCDRC In Boiler Blast Case

- November 14, 2025

In a notable ruling, the Supreme Court has allowed the insurance claim of a sugar factory whose boiler exploded in 2005, rejecting the insurer’s attempt to deny liability based on defects found only after the incident. A Bench of Justice P.S. Narasimha and Justice Manoj Misra held that insurers cannot avoid paying claims by relying on latent defects discovered during post-accident surveys, noting that doing so would defeat the purpose of insurance contracts.

“A subsequent discovery of damage or corrosion cannot be a ground to repudiate an insurance claim, as it would defeat the very purpose of the insurance contract,” the Court observed, adding that it is the insurer’s duty to carry out necessary checks before issuing the policy, not after an accident.

BACKGROUND:

The case arose from a boiler explosion on May 12, 2005, at the appellant’s sugar factory. The boiler, insured with National Insurance Co. Ltd. under a Boiler and Pressure Plant Policy for ₹1.60 crore, suffered substantial damage. Upon investigation, the insurer’s surveyor attributed the incident to corrosion and deterioration in decades-old boiler tubes. Citing Exclusion Clause 5, which excludes damage caused by wear, corrosion or deterioration unless those defects trigger an explosion, the insurer rejected the claim.

The Maharashtra State Consumer Commission, however, in 2012 found the rejection unjustified and awarded ₹49 lakh for deficiency in service. This decision was overturned by the National Consumer Disputes Redressal Commission (NCDRC) in 2020, which accepted the insurer’s contention that the loss was barred by the exclusion clause. The factory appealed to the Supreme Court, challenging the NCDRC’s reversal.

Appellant’s Contention:

The appellant argued that the boiler had a valid fitness certificate under the Boilers Act and that the insurer had conducted its own evaluation before issuing the policy. Any defects that surfaced post-explosion were therefore hidden and could not form the basis of rejection. Crucially, the appellant asserted that the loss resulted from an explosion, a fact never denied by the insurer.

Insurer’s Defense:

The insurer argued that corrosion, not an explosion, caused the boiler failure, and therefore the claim fell under the policy’s exclusion clause. It relied on the surveyor’s findings to say that any underlying defect— even if discovered only after the accident—removed its liability.

Court’s Observations:

The Supreme Court rejected this argument, holding that an insurer cannot rely on defects it failed to identify during its own checks before issuing the policy.

“It is expected that an insurer would accept a proposal of insurance on being satisfied with the condition of the subject matter of insurance. Otherwise, the purpose of an insurance, which is to tide over financial implications of an unforeseen event such as an accident, would stand frustrated.” the Bench noted.

The Court reiterated that insurers can deny claims only on specific grounds—either by showing that the insured hid important information or by proving that the policy clearly excludes the claim. In this case, neither condition was met. The insurer did not allege any fraud, misrepresentation, or non-disclosure, and it also did not show that the insured blocked inspection or gave false information.

“Mere discovery of corrosion on underlying parts while making a survey is not conclusive to hold that there was infraction of duty to make a fair disclosure for the simple reason that those underlying parts got noticed only because tubes slipped off on account of the explosion.” the Court observed.

The Bench also noted that the appellant’s claim that an explosion had occurred was never disputed by the insurer.

“Appellant’s specific case was that an explosion took place resulting in tubes slipping off from boiler’s main body. This plea of appellant was not traversed. Even survey report was placed on record at the appellate stage and not before. There is no plea that insured played fraud upon the insurer either by not allowing an inspection or by submitting a false data. All of this shows that the first respondent was interested in somehow defeating the claim of the appellant not on facts but on pleas taken as an after-thought.” the court stated.

Court’s Ruling:

The Court held that the insurer had failed to demonstrate that the exclusion clause actually applied, and said that such clauses must be interpreted strictly and cannot be used without clear and definite evidence.

The Supreme Court allowed the appeal, cancelled the NCDRC’s 2020 decision, and restored the sugar factory’s right to compensation under the insurance policy.

Since the NCDRC had not decided how much compensation should be given, the Court sent the case back to it only to fix the amount. All other objections were rejected, and the Court said the insurer could not deny the claim based on defects found only after the explosion.

Advocate for the Petitioner: Mr. Shekhar G. Devasa, Sr. Adv. Ms. Rajshri A. Dubey, Adv. Mr. Abhishek Chauhan, Adv. Mr. Amit P. Shahi, Adv. Mr. H.B. Dubey, Adv. Mr. Amit Kumar, Adv. Mr. Shashi Bhushan Nagar, Adv. Ms. Jashmita, Adv. Mr. Prashant, Adv. Mr. Gaurav sharma, Adv. Mr. Yogesh Malhotra, Adv. Mr. Ashutosh Dubey, AOR

Advocate for the Respondent: Mr. Gaurav Sharma, AOR Mr. Sushant Kishore, Adv. Mr. Adarsh Dubey, Adv. Mr. Siddharth Dharmadhikari, Adv. Mr. Aaditya Aniruddha Pande, AOR

Sign up for free and be the first to get notified about curated content just for you.